Key Takeaways

- Most financed cars need full coverage while the loan is active.

- Full coverage usually means liability, collision, and comprehensive insurance.

- Lenders require it to protect the car that secures the loan.

- Gap insurance can help if the car is totaled and you owe more than the insurer pays.

- You can usually reduce coverage only after the lienholder is removed and the loan is fully paid.

Introduction

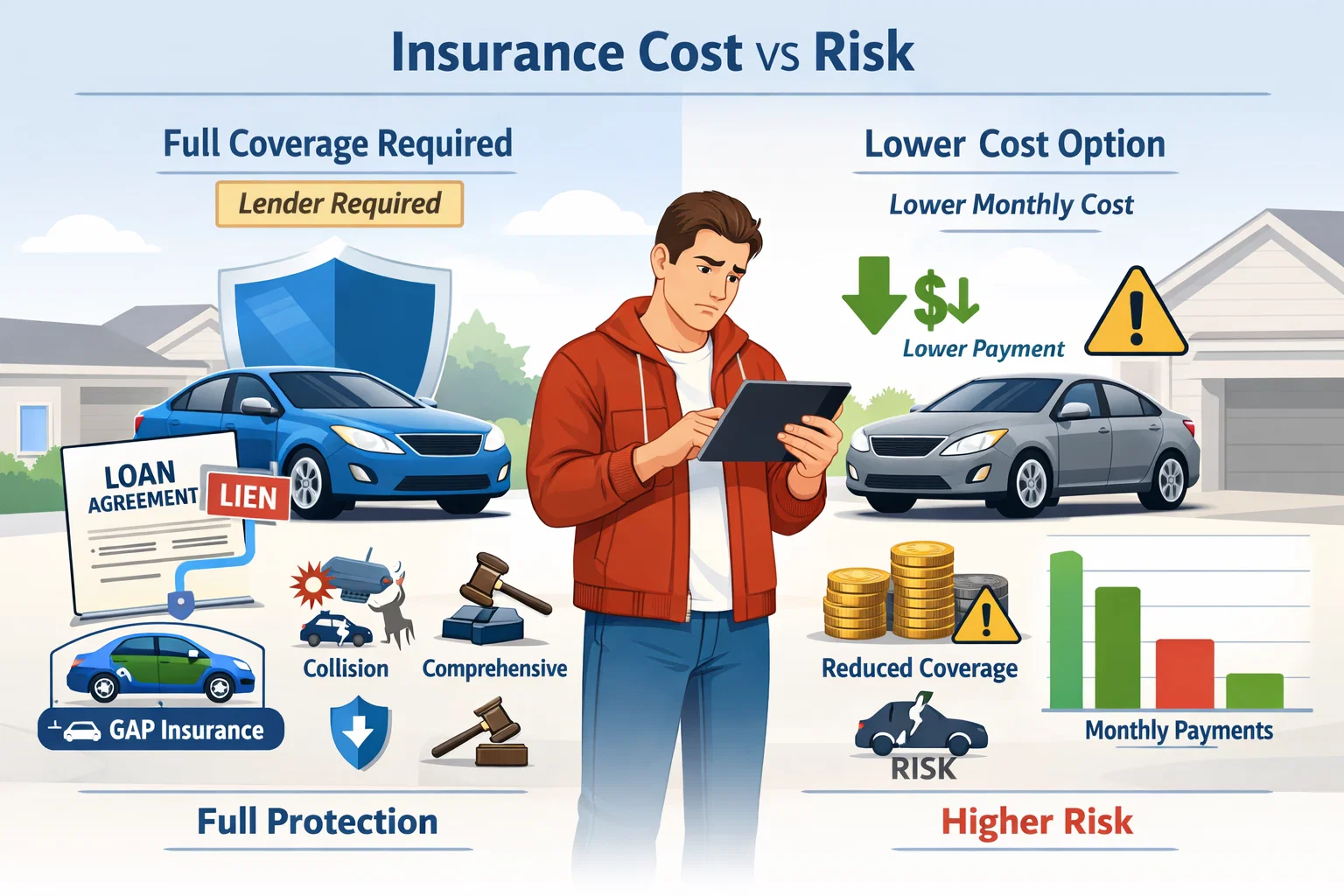

Yes, you usually need full coverage on a financed car because most lenders require collision and comprehensive insurance until the loan is fully paid off.

That requirement protects the lender’s investment and helps protect you from paying for a damaged or totaled car while you still owe money on the loan.

Full coverage on a financed car usually includes liability insurance, collision insurance, and comprehensive insurance, while gap insurance may be useful when the loan balance is higher than the car’s actual value.

What Is Full Coverage Auto Insurance?

Full coverage auto insurance is not one special policy name. Full coverage is a common term used to describe a car insurance policy that combines several important protections. In most cases, full coverage includes liability insurance, collision insurance, and comprehensive insurance. Liability insurance pays for damage or injuries you cause to others. Collision insurance pays for damage to your financed car after a crash. Comprehensive insurance pays for non-collision losses such as theft, vandalism, hail, fire, or falling objects.

A financed car needs more than liability-only minimum insurance in most cases because the lender wants the vehicle itself protected. That is why full coverage needs are usually tied to the loan agreement and not only to state law. Full coverage auto insurance gives broader protection than liability only, which is why it is the standard choice for a financed vehicle.

How much does full coverage auto insurance cost?

Full coverage auto insurance cost depends on several factors. The biggest factors are the car’s value, the driver’s age, location, claims history, credit profile where allowed, deductible amount, and coverage limits. A newer financed car usually costs more to insure than an older car because repair and replacement costs are higher. A lower deductible raises the premium, while a higher deductible lowers the premium but increases out-of-pocket cost after a claim. A financed car with strong safety features may cost less to insure than a financed car with high repair costs or theft risk.

Car Loan Insurance Requirements

Car loan insurance requirements usually come from the lienholder. The lienholder is the lender with a legal interest in the vehicle until the loan is paid in full. State law may only require liability insurance, but a lender usually requires more than the legal minimum. Most lenders want a policy that includes collision insurance and comprehensive insurance, and some lenders may set maximum deductible limits as part of the loan agreement.

These car loan insurance rules exist because the vehicle serves as collateral for the loan. If the financed car is damaged, stolen, or totaled, the lender still expects the balance to be paid. Insurance helps reduce that risk. This is why financed car coverage is different from insurance on a car you own outright.

Do Lenders Require “Full Coverage” on Financed Cars?

Yes, lenders usually require full coverage on financed cars. A lender does not want the financed vehicle protected by liability insurance alone because liability insurance does not pay to repair or replace your own car. A financed car full coverage policy gives protection against accident damage and many non-collision losses.

Protecting the Lender’s Investment

The financed car is the lender’s collateral. If the car is heavily damaged, the lender’s financial position is at risk. Collision and comprehensive coverage protect the physical vehicle. That makes full coverage necessary from the lender’s point of view. The lender is not trying to increase your insurance bill without reason. The lender is trying to protect the asset that supports the loan.

Protecting the Driver’s Financial Security

Full coverage financed vehicle insurance protects the driver too. If you only carry liability insurance and your financed car is stolen, burned, or totaled in a crash, you may still owe the lender the remaining loan balance with no usable car. Full coverage reduces that risk. A financed car protection plan with collision and comprehensive insurance helps protect against major financial hardship after a loss.

Why Do You Need Full Coverage on a Financed Car?

You need full coverage on a financed car for three main reasons. First, the loan agreement usually requires it. Second, it protects your finances if the car is damaged, stolen, or destroyed. Third, it helps avoid default problems with the lender. A financed vehicle insurance policy that only carries liability insurance leaves a major gap in protection. That gap can become very expensive after an accident or a total loss.

A financed car often represents a large monthly obligation. Removing key coverage may save money in the short term, but it can create a much larger problem later. That is why full coverage required on a financed car is usually the safer and more practical choice.

You Can Also Read

How Invoice Financing Helps Small Businesses Improve Cash Flow Quickly

Why Lenders Require Full Coverage Insurance On A Financed Car Explained

Why Choosing Roofing Companies That Finance Can Help Avoid Upfront Costs

What Happens If You Don’t Have Full Coverage on a Financed Car?

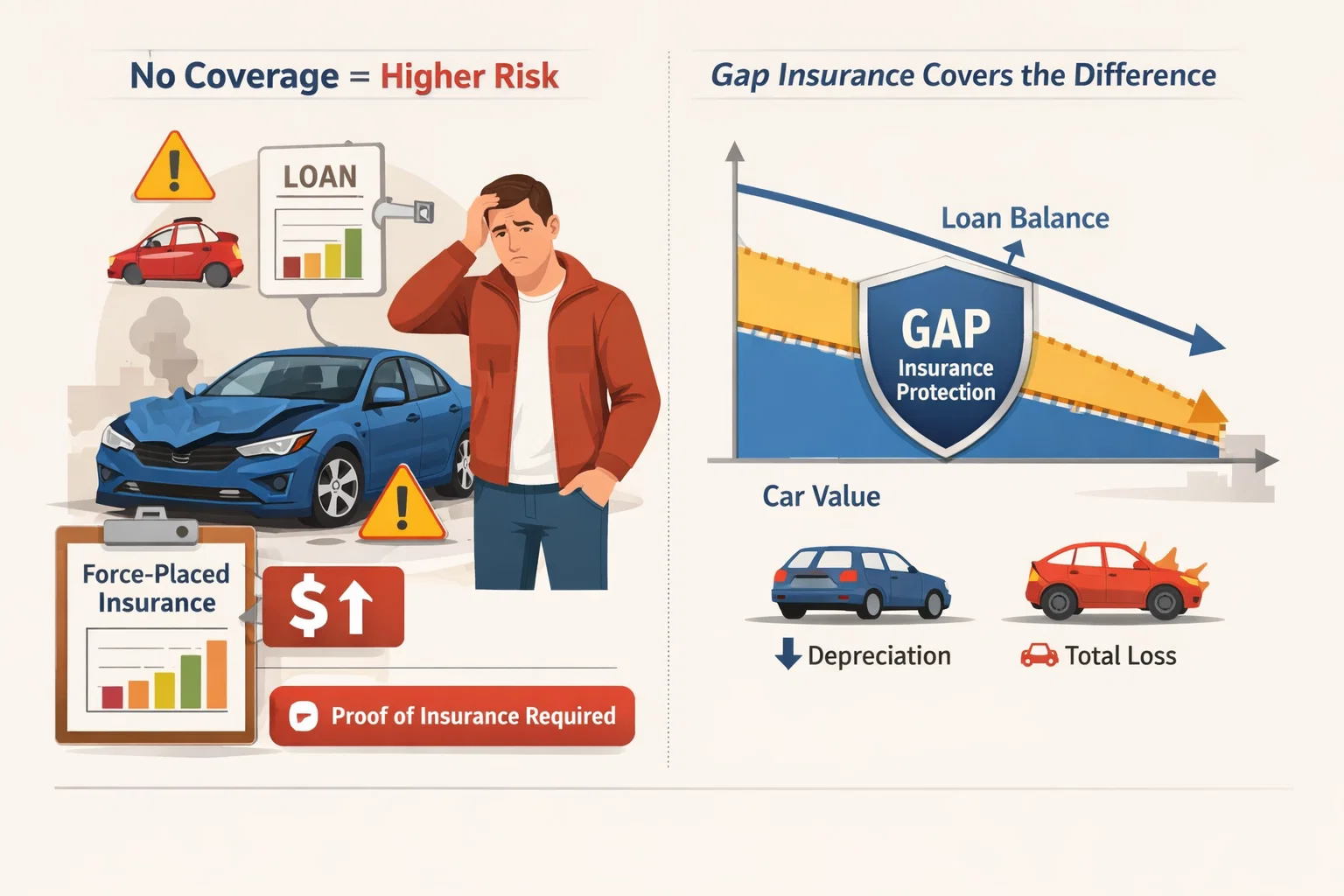

If you do not have full coverage on a financed car, the lender may treat that as a violation of the loan agreement. In many cases, the lender can buy Force-Placed Insurance or collateral protection insurance and add the cost to your loan payment or balance. This type of coverage usually protects the lender, not you. It can be expensive and limited compared with a regular full coverage auto insurance policy.

You may also receive warning notices asking for proof of insurance. If you do not respond, the lienholder can act without waiting for your permission. That makes a lapse in financed car insurance more than just an insurance issue. It can become a loan issue.

The Role of Gap Insurance in Financed Cars

Gap Insurance is different from full coverage, but it can be very important for a financed car. Full coverage helps pay for physical damage or loss to the vehicle. Gap Insurance helps if the insurer pays less than the remaining loan balance after a total loss.

Why Gap Insurance Matters

Cars lose value faster than many loan balances go down. That means a financed car can become worth less than what you still owe. If the car is totaled, the insurance company usually pays the actual cash value of the vehicle, not the full unpaid loan balance. Gap insurance matters because it covers that difference. This is especially useful with small down payments, long loan terms, rolled-over negative equity, or fast vehicle depreciation.

Lender Requirements and Recommendations

Some lenders require gap insurance, while others strongly recommend it. It is not always mandatory, but it is often a smart choice for a financed vehicle with a high loan-to-value ratio. A lender may mention gap insurance during the loan process or include it as part of dealer financing paperwork.

How do I buy gap insurance?

You can usually buy gap insurance through the dealership, the lender, or your car insurance provider if offered. Some buyers choose it at the time of purchase. Others add it later after reviewing the loan balance and vehicle value. The best time to consider gap insurance is early in the loan when the risk of being underwater is highest.

Insurance Coverage Required by Lenders

Lenders usually require four types of insurance to be reviewed closely: liability insurance, collision insurance, comprehensive insurance, and in some cases gap insurance. Liability coverage is often required by state law. Collision and comprehensive are usually required by the lender. Gap insurance may be required or recommended depending on the loan structure.

Are the coverage requirements different when financing a used car?

The main lender requirements are usually similar when financing a used car. A lender still wants collision and comprehensive insurance on a used financed car because the vehicle still secures the loan. The biggest difference is usually cost and value, not the basic requirement. Older financed cars may cost less to insure than new financed cars, but the lender still wants full coverage if the loan remains active.

Do You Need Full Coverage Insurance on a Used Financed Car?

Yes, you usually need full coverage insurance on a used financed car if the lender requires it. The age of the vehicle does not remove the lender’s right to demand full coverage while the loan exists. A used car financed through a lender is still collateral. That is why comprehensive and collision coverage usually stay in place until payoff.

What Full Coverage Auto Insurance Really Means

Full coverage auto insurance really means broad protection rather than one single policy label. It usually means you have liability insurance for other people’s losses, collision insurance for crash damage to your car, and comprehensive insurance for non-collision damage to your car. Some drivers add roadside assistance, rental reimbursement, or uninsured motorist coverage, but those are separate options. Full insurance coverage on a financed car is mainly about protecting the vehicle itself along with meeting financial responsibility rules.

When You Can Drop Full Auto Insurance Coverage

You can usually drop full auto insurance coverage after the financed car is paid off and the lienholder’s interest ends. At that point, the decision becomes yours instead of the lender’s. That does not always mean you should drop coverage right away. It means the requirement changes from a contract issue to a risk-and-cost decision.

Evaluate Your Car’s Value

Start by checking the car’s actual market value. If the car is worth very little and the cost of collision and comprehensive insurance is high, carrying full coverage may no longer make financial sense. If the car still has solid value or would be expensive for you to replace, keeping full coverage may still be smart.

Balance Risk and Cost

Balancing risk and cost is the key decision once the loan is gone. Ask whether you could afford to replace the car if it were stolen or totaled. If the answer is no, broader coverage may still be worth paying for. If the answer is yes, reducing coverage may be reasonable.

Used or Pre-Owned Financed Car Considerations

Used or pre-owned financed car considerations matter most after payoff. An older car may not justify high premiums for collision and comprehensive coverage. Still, some older vehicles hold value well or remain expensive to replace in today’s market. The best decision depends on real replacement cost, not only age.

Can You Drop Full Coverage Insurance on a Financed Car?

You can cancel full coverage insurance on a financed car, but that does not mean you are allowed to do it under the loan agreement. If you remove required coverage while the loan is active, you may violate the contract. The lienholder can respond by requiring proof of insurance, purchasing force-placed insurance, or treating the issue as a default problem.

How Does My Lienholder Know If I Drop Full Coverage?

Your lienholder usually knows through insurance tracking systems, policy notices, or direct communication from the insurer. Because the lienholder has a legal interest in the financed vehicle, insurance companies often notify the lienholder when coverage changes, lapses, or is canceled. That means dropping coverage quietly is rarely realistic for long.

When Should You Drop Full Coverage Insurance on a Financed Car?

You should usually drop full coverage insurance on a financed car only after the loan is fully paid and after you compare the premium against the car’s current value. If the car still has strong value, you may choose to keep full coverage even without a lender requirement. If the car has low value and you can absorb a loss, liability-only coverage may become the more practical choice.

What Happens After I Pay Off My Financed Vehicle?

After you pay off your financed vehicle, the lienholder no longer has a security interest in the car. That means the lender can no longer require collision and comprehensive insurance. Your insurance company should update the policy to remove the lienholder. At that point, you decide whether to keep full coverage auto insurance, reduce coverage, or change carriers.

Your Options Once You Pay Off Your Financed Car

You have three basic options after payoff. You can keep full coverage for continued protection. You can reduce coverage to liability only if the vehicle’s value is low and you can handle replacement risk. Or you can adjust deductibles, add or remove optional protections, and shop for better pricing. The best option depends on the car’s value, your savings, and your tolerance for risk.

How to Buy Insurance for a Financed Car

To buy insurance for a financed car, compare quotes from insurers, choose the required liability, collision, and comprehensive coverage, set deductibles that meet lender limits, and list the lienholder on the policy. It is smart to review the declarations page before finalizing the policy. Make sure the policy matches the loan agreement and includes any coverage tools or protections you want for the financed vehicle.

How GEICO Car Insurance Helps You Meet Lender Requirements

GEICO Car Insurance can help financed-car drivers meet lender requirements by offering liability insurance, collision insurance, and comprehensive insurance in one policy setup. GEICO also provides support features such as My Account, Claims and Roadside Help, Web and Mobile access, and other tools and resources that make policy management easier. For drivers comparing policies, the main value is that the policy can be shaped to match lender coverage needs while staying practical for day-to-day use.

Ways to save on auto insurance for financed vehicles

There are several ways to save on auto insurance for financed vehicles without removing required coverage. Raise the deductible if the lender allows it. Compare quotes from different insurers. Bundle auto with home or life coverage when discounts apply. Maintain a clean driving record. Ask about safe-driver, anti-theft, low-mileage, or autopay discounts. The goal is to lower the premium while still keeping the full coverage lender rules require.

What kind of coverage do you need for a financed car?

A financed car usually needs liability insurance, collision insurance, and comprehensive insurance. Some drivers may also need underinsured and uninsured motorist coverage depending on state law, lender expectations, or personal risk concerns.

Collision insurance

Collision insurance pays for damage to your financed car after a crash, whether the accident involves another vehicle or an object such as a pole or guardrail. This coverage is one of the core protections most lienholders require.

Comprehensive insurance

Comprehensive insurance covers non-collision damage such as theft, vandalism, flood, hail, falling objects, and animal strikes. This protects the financed vehicle from losses that are not tied to a standard road accident.

Bodily injury liability coverage

Bodily injury liability coverage pays for injuries you cause to other people in an accident. This is a core part of car insurance and is required by law in most states.

Underinsured and uninsured motorist coverage

Underinsured and uninsured motorist coverage helps protect you if another driver causes a crash and has little or no insurance. This coverage is not the same as collision or comprehensive, but it can be an important part of a strong financed car insurance plan.

Full coverage auto insurance

Full coverage auto insurance usually means liability plus collision plus comprehensive. That is why the phrase full coverage financed car insurance appears so often in car loan discussions. It is the combination that protects both the lender and the driver.

Do I need gap insurance on a financed car?

You do not always need gap insurance on a financed car, but many borrowers benefit from it. If you put little money down, chose a long loan term, or financed more than the car’s market value, gap insurance can be very valuable. It is most useful when depreciation is likely to create a difference between the insurer payout and the remaining loan balance.

Insurance for Leased Car vs. Owned Car: What You Need to Know

Insurance for leased car vs. owned car works differently in some key ways. Both leased and financed cars usually require full coverage, but leased cars often come with stricter rules. A lease company may require lower deductibles, higher liability limits, or more exact insurance terms than a standard lender.

Leased and financed cars both require full coverage, but there are some key differences.

The main difference is control and contract detail. A financed car moves toward ownership once the loan is paid. A leased car never becomes yours unless you buy it later. Lease agreements often set tighter insurance conditions, while financed-car insurance focuses more on protecting collateral during the loan.

Insuring a leased car

Insuring a leased car usually means carrying liability, collision, and comprehensive coverage with contract-approved limits and deductibles. Lease companies may be stricter than lenders because they fully own the vehicle during the lease term.

Find the best car insurance

To find the best car insurance, compare premium, deductible options, claims support, financial strength, policy features, and how well the insurer handles financed or leased vehicle requirements. Price matters, but policy fit matters too.

The difference between leasing and buying a car

Buying a car with a loan leads to ownership after payoff. Leasing gives you use of the car for a set term without building full ownership unless you purchase it later. This difference affects long-term insurance decisions. A financed car can move to liability-only coverage after payoff if you choose. A leased car stays under lease rules until the lease ends.

Summary

Yes, you usually need full coverage on a financed car because most lenders require collision and comprehensive insurance until the loan is paid off. Full coverage helps protect both the lender’s investment and your own finances if the car is damaged, stolen, or totaled. The article explains what full coverage includes, how gap insurance helps, and what can happen if your policy lapses. It also covers when you can drop full coverage, how leased-car insurance differs, and what your options are after the car is fully paid off.

FAQs

1. Do I need full coverage on a financed car?

Yes, most lenders require full coverage on a financed car until the loan is fully paid off.

2. What does full coverage on a financed car include?

It usually includes liability insurance, collision insurance, and comprehensive insurance.

3. What happens if I drop full coverage on a financed car?

The lender may add force-placed insurance, increase your costs, or treat it as a loan agreement violation.

4. Do I need gap insurance on a financed car?

Not always, but it can help if you owe more on the loan than the car is worth after a total loss.

5. Can I remove full coverage after I pay off my car?

Yes, once the loan is paid off, you can choose to reduce coverage based on the car’s value and your risk.