Introduction

Finance of America Reverse (FOAR) is a reverse mortgage lender that helps eligible homeowners convert home equity into cash while staying in the home and without taking on required monthly mortgage payments on the reverse mortgage itself.

In practice, finance of america reverse products are used for retirement income planning, home renovation financing, debt management, and aging in place.

The main parts include loan eligibility, counseling requirements, payment options, costs, repayment rules, and lender-specific offerings such as HECMs, HomeSafe, HomeSafe Second, and other proprietary solutions.

This article follows your requested structure and keyword focus while grounding the lender and reverse-mortgage sections in current lender, HUD, FHA, FTC, SEC, and Money source material.

Understanding Reverse Mortgages

How Reverse Mortgages Work

A reverse mortgage is a loan for older homeowners that turns part of home equity into available cash. The borrower keeps title to the home and can remain there as a primary residence, but the loan becomes due when the home is sold, the borrower moves out permanently, the last borrower dies, or loan obligations are not met. For HECMs, HUD states that borrowers may remain in the home indefinitely as long as property taxes, homeowners insurance, and other loan obligations stay current.

Benefits of Reverse Mortgages

There are 5 main reverse mortgage benefits. A reverse mortgage can create a supplemental income stream, remove a required monthly mortgage payment on an existing mortgage if proceeds are used to pay it off, support long term care funding, provide a financial safety cushion, and help with strategic retirement planning. Finance of America describes reverse mortgages as a way to access home equity without adding monthly mortgage payments, and HUD says HECM proceeds can be used for maintenance, repairs, or general living expenses.

Implications of Reverse Mortgages

A reverse mortgage is not free money. Interest accrues on the outstanding balance, fees may be added to the balance, home equity declines over time, and the borrower must still pay property taxes, homeowners insurance, and maintenance costs. FTC guidance warns consumers to understand the costs, risks, and cancellation rights before signing.

Key Takeaways

Finance of america reverse is a lender in the reverse mortgage market, not a general-purpose bank brand. Reverse mortgages can improve cash flow for eligible homeowners, but reverse mortgages can reduce future home equity and change estate planning outcomes. HECMs are FHA-insured and regulated. Proprietary reverse mortgages may offer higher-value loan options or different age rules. Lender comparison matters because rates, fees, availability, and user experience vary by product and by state.

How Reverse Mortgages Differ From Traditional Mortgages

Traditional mortgages require the borrower to make monthly payments that reduce principal over time. Reverse mortgages generally do the opposite: the lender advances funds to the borrower, the balance usually grows over time, and repayment is deferred until a maturity event. Traditional mortgages focus on home purchase or refinance. Reverse mortgages focus on home equity unlocking, retirement income planning, and aging in place.

Types of Reverse Mortgages

Home Equity Conversion Mortgages (HECMs)

A Home Equity Conversion Mortgage (HECM) is the main FHA-insured reverse mortgage product. HUD explains that HECMs are designed for seniors and include borrower protections such as required counseling and federal insurance through the FHA. HECMs are often the best-known Home Equity Conversion Mortgages for Seniors.

Proprietary Reverse Mortgages

Proprietary reverse mortgages are private loans offered by lenders instead of the FHA. Finance of America offers proprietary reverse mortgage products under the HomeSafe brand, including HomeSafe and HomeSafe Second. Finance of America states that some HomeSafe products can go as high as $4 million for qualifying properties, and some proprietary products can have a minimum age lower than 62 depending on state and product rules.

Single-Purpose Reverse Mortgages

Single-purpose reverse mortgages are typically offered by nonprofit organizations or government agencies and are limited to a defined use such as repairs or taxes. They are less common than HECMs and proprietary reverse mortgages. FTC consumer guidance still treats them as a form of reverse mortgage that needs careful review before borrowing.

Eligibility Requirements and Qualification Factors

Eligibility depends on the product. For HECMs, the standard age threshold is 62 or older, the home must be the primary residence, the borrower must complete HUD-approved counseling, and the borrower must show the ability to meet ongoing property charges. Finance of America says some proprietary HomeSafe products may allow eligibility as young as 55, subject to lender rules and state restrictions, while Massachusetts, New York, and Washington use 60 for certain HomeSafe products and North Carolina and Texas use 62.

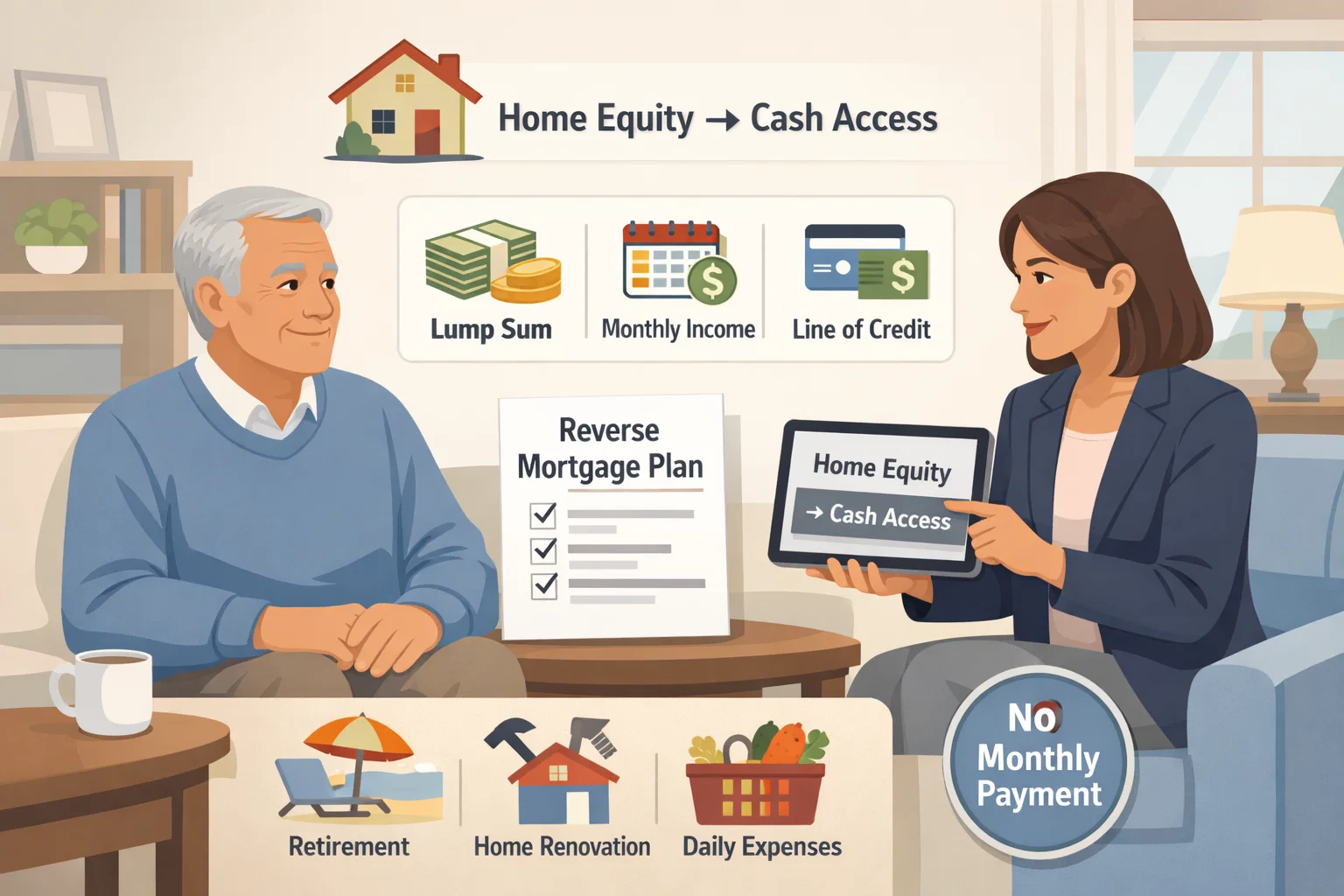

Payment Options and Distribution Methods

Reverse mortgage proceeds can be distributed through a lump sum, monthly advances, a line of credit, or a combination, depending on the product. Adjustable-rate loans commonly support line-of-credit flexibility, while fixed rate reverse products often lean toward lump-sum structures. The exact payment design affects interest accrual, available cash, and long-term loan growth.

How Reverse Mortgage Funds Are Commonly Used

Borrowers commonly use reverse mortgage funds for 5 purposes: paying off an existing mortgage, covering daily expenses, funding home renovation financing, handling medical or care costs, and improving retirement liquidity. Finance of America’s educational materials position reverse mortgages as tools for supplementing household cash flow, managing long-term risks, and supporting retirement planning.

Costs and Fees Associated with Reverse Mortgage Loans

Reverse mortgage costs can include origination fees, closing costs, mortgage insurance premiums for HECMs, interest charges, and sometimes servicing-related costs. Finance of America’s site discloses that the lender may charge an origination fee, mortgage insurance premium where applicable, closing costs, and servicing fees, with those amounts typically added to the loan balance. That is why a reverse mortgage calculator and direct lender quote matter before signing.

Advantages and Risks for Reverse Mortgage Borrowers

The 4 main advantages are cash-flow relief, housing wealth conversion, no required monthly reverse mortgage payment, and the ability to stay in the home. The 4 main risks are shrinking equity, compound interest growth, loss of the loan if taxes or insurance are not paid, and reduced inheritance for heirs. The product can work well as a retirement income optimizer, but only if the borrower understands both the flexibility and the long-term cost.

Reverse Mortgage vs. Other Home Equity Options

Refinancing an Existing Mortgage

A refinance replaces an existing loan with a new one and usually requires monthly payments. A reverse mortgage can eliminate that payment requirement if proceeds pay off the old mortgage, but the reverse balance grows instead of amortizing down.

Home Equity Loan

A home equity loan gives the borrower a lump sum and fixed repayment schedule. A reverse mortgage usually delays repayment, which is why it can fit some retirees better than a standard second mortgage.

Home Equity Line of Credit (HELOC)

A Home equity line of credit (HELOC) offers revolving borrowing, but it usually requires monthly payments and underwriting tied more directly to income and debt ratios. A reverse mortgage line of credit can be easier for some older borrowers who need payment flexibility, though it comes with its own rules and costs.

Cash-Out Refinance

A Cash-out refinance replaces the first mortgage with a larger one and gives the borrower cash at closing. It can work well for homeowners with strong income and good rates. A reverse mortgage fits a different borrower profile: older homeowners who want home equity access without a new monthly payment.

Downsizing to a Smaller Home

Downsizing can free cash and reduce housing expenses. A reverse mortgage for purchase, including HECM for Purchase and Finance of America’s HomeSafe for Purchase, can serve homeowners who want to move into a new primary residence while preserving more liquid assets.

Application Process for a Reverse Mortgage

The application process usually has 6 steps: lender consultation, counseling, application, appraisal, underwriting, and closing. Finance of America offers contact-first intake and quote tools rather than a simple fully self-serve online application flow. The company’s calculator and start pages route the borrower to a reverse mortgage specialist for a more detailed estimate.

What Happens at the End of a Reverse Mortgage?

Sell the Home

Selling the home is the most common end-of-loan path. The reverse mortgage balance is repaid from sale proceeds, and any remaining equity belongs to the borrower or heirs. HECMs are non-recourse loans, so qualified borrowers or heirs do not owe more than the home’s value at repayment.

Keep the Home

Heirs can keep the home by paying off the balance with cash or a new refinance. This path matters for families using reverse mortgages as part of estate planning integration or legacy preservation.

Sign Over the Title and Complete a Deed in Lieu of Foreclosure

A deed in lieu can resolve the debt if heirs or the estate do not want to keep the home. This option may avoid a longer foreclosure process, though legal advice is still wise.

Do Nothing

If the estate does nothing, the servicer can begin its collections and foreclosure timeline after the loan becomes due and payable. Ignoring notices is usually the worst path.

Getting a Reverse Mortgage: Next Steps

Start with HUD-approved counseling and compare more than one lender. Review lender information, rates, fees, product fit, service support, and state availability. A shopper should use both educational tools and direct quotes. Reverse mortgage consumer information, housing counselor information, and reverse mortgage details are worth reviewing before choosing a loan.

Finance of America Reverse Mortgages Review

At a Glance

Finance of America says it is a division of Finance of America Reverse LLC, licensed nationwide under NMLS ID 2285, with a Tulsa, Oklahoma address on its site. The company markets itself as an industry-leading reverse mortgage lender and says its recent acquisition of certain American Advisors Group assets helped expand its retail and wholesale platforms. Not all products are available in all states, and the company says it does not do business as Finance of America in California, New Mexico, New York, and Oklahoma.

Finance of America Reverse: Pros and Cons

Pros Explained

Wide Variety of Reverse Mortgage Solutions

Finance of America offers HECMs, HomeSafe, HomeSafe Second, reverse mortgage estimate tools, educational resources, and purchase-focused products. BBB profiles for several branches list HECM, HomeSafe, and HomeSafe Second among its reverse mortgage solutions. (BBB)

All Customers Receive a Direct Line to a Support Agent

Finance of America’s contact pages and quote pages direct users to call licensed specialists and support teams. The company leans toward human-assisted service rather than a pure self-serve digital funnel.

Ability to Match Compatible Roommates to Help Retirees Earn Extra Income

Finance of America has promoted Silvernest Home-Sharing as a way to help retirees earn extra income by sharing unused space. That makes it a distinctive add-on compared with lenders that only offer loan products.

Cons Explained

No Online Reverse Mortgage Applications

The lender offers online forms and estimate tools, but the process still centers on speaking with a specialist. That is less convenient for borrowers who want a full end-to-end digital application experience. (Finance of America)

Recent SEC Closures Suggest Challenges

It is more accurate to say that Finance of America remains active in SEC filings than to say it has shut down. Current SEC filings exist for Finance of America, and a 2025 SEC-linked press release announced a strategic relationship between Onity Group and Finance of America Reverse. That suggests an operating business with ongoing transactions, though public filings still warn about market and operational risks. (SEC)

No Information About Interest Rates or Terms Online

Finance of America’s public pages promote estimates and consultations, but detailed rate sheets and full pricing terms are not posted in a way that lets borrowers compare all offerings instantly online. That means a direct quote is necessary. (Finance of America)

Finance of America Reverse Mortgage Offerings

HECMs

Finance of America offers HECMs, the FHA-insured Home Equity Conversion Mortgage product. These are the standard reverse mortgages most consumers first encounter. (HUD)

HomeSafe for Purchase

Finance of America offers reverse mortgage purchase solutions for buyers who want to use home equity strategies when moving into a new principal residence. This product category sits alongside HECM for Purchase concepts in the broader market. (Finance of America)

HomeSafe Second

HomeSafe Second is Finance of America’s proprietary second-lien reverse mortgage product. The company lists it in its product family and help-center content. (Finance of America)

HomeSafe Standard

HomeSafe Standard refers to the core proprietary HomeSafe structure mentioned in your prompt and reflected in lender product framing around HomeSafe solutions. It sits apart from HECMs and is not FHA-insured. (Finance of America)

HomeSafe Jumbo Reverse Mortgage

Finance of America describes HomeSafe jumbo reverse mortgage options for higher-value homes. Its educational material says certain HomeSafe products may support loans up to $4 million for qualifying borrowers and properties. (Finance of America)

EquityAvail Retirement Mortgage

EquityAvail Retirement Mortgage appears in your prompt as one of the offerings to cover. It fits the proprietary reverse mortgage theme and the lender’s retirement-focused positioning.

Silvernest Home-Sharing

Silvernest is the home-sharing concept tied to helping retirees earn extra income from extra rooms. It is not a reverse mortgage itself, but it can complement one.

Principal Loan Limit

The Principal loan limit is the maximum amount available under a reverse mortgage calculation before mandatory obligations and closing costs are netted out. For HECMs, the principal limit depends on borrower age, expected interest rates, and the lesser of appraised value or the FHA lending cap. For proprietary reverse mortgages, the lender’s own rules apply. (HUD)

Finance of America Reverse Mortgage Pricing

Finance of America reverse mortgage pricing is quote-based. The lender’s calculator page says borrowers should connect with a licensed reverse mortgage specialist for a detailed no-obligation estimate covering loan options, rates, and fees. That means finance of america reverse rates are not fully transparent from public pages alone. (Finance of America)

Finance of America Reverse Mortgage Financial Stability

Finance of America continues to operate, file with the SEC, and participate in reverse mortgage transactions. The company’s SEC materials show ongoing reporting activity, and the 2025 Onity relationship announcement indicates continued market participation. That said, reverse mortgage lending remains sensitive to housing values, rates, securitization markets, and compliance costs, so financial stability should always be judged with current filings, not branding alone. (SEC)

Finance of America Reverse Mortgage Accessibility

Availability

Finance of America says it is licensed nationwide, but not all products and options are available in all states. The site also says the company does not do business as Finance of America in CA, NM, NY, and OK. (Finance of America)

Contact Information

Finance of America’s main contact page lists (800) 841-5166 for help learning which home equity solution may fit. Other lead and estimate pages show specialist numbers such as (800) 820-1715 and (800) 841-4626, which indicates multiple intake channels. The site footer lists 8023 East 63rd Place, Suite 700, Tulsa, OK 74133. (Finance of America)

User Experience

The user experience is built around agent support, quote requests, educational pages, and calculators instead of a pure online reverse mortgage portal. Borrowers who prefer phone guidance may like that. Borrowers who want instant online answers 24/7 and full digital completion may not. (Finance of America)

Finance of America Reverse Mortgage Customer Satisfaction

Customer satisfaction is mixed but not alarming. Finance of America’s homepage includes positive testimonial-style reviews, and BBB business profiles show A+ ratings for several listed locations, while BBB complaints pages show complaint activity over the last three years. That combination suggests a lender with scale, active servicing, and normal complaint volume rather than a complaint-free lender. (Finance of America)

Who’s Eligible for a Finance of America Reverse Mortgage?

Age

For HECMs, the standard age is 62+. For some HomeSafe proprietary products, Finance of America says the minimum age may be 55 depending on product and state. (Finance of America)

Other Requirements

Other requirements include primary-residence occupancy, home equity, property condition, financial assessment, and ongoing payment of taxes and homeowners insurance. HECMs require counseling; proprietary products may have lender-specific counseling requirements. (HUD)

How Do You Repay a Reverse Mortgage From Finance of America Reverse?

Repayment happens when the home is sold, the borrower moves out permanently, the last borrower dies, or loan terms are not met. The balance is usually paid from sale proceeds, refinance funds, or estate resources. HECMs are non-recourse loans, so repayment does not exceed the home value under program rules. (HUD)

Is Finance of America Reverse a Reputable Lender?

Yes. Finance of America Reverse appears to be a legitimate and active reverse mortgage lender. It is licensed nationwide, lists NMLS information publicly, maintains active contact and quote channels, appears in SEC-linked materials, and is BBB-accredited in several profiles. Reputation still depends on product fit, service quality, and how well a borrower understands the loan. (Finance of America)

How to Apply for a Finance of America Reverse Mortgage

Start with a consultation or estimate request, complete the required counseling if you are applying for a HECM, gather income and property documents, complete the lender application, wait for appraisal and underwriting, then review final disclosures before closing. Borrowers looking for finance of america reverse login, finance of america reverse payoff request, or finance of america reverse mortgage payoff details usually need to contact servicing directly rather than relying only on public marketing pages. (Finance of America)

Finance of America Reverse Mortgage FAQ

What is Finance of America Reverse?

Finance of America Reverse is a reverse mortgage lender operating as a division of Finance of America Reverse LLC and focused on home equity solutions for older homeowners. (Finance of America)

Is Finance of America Reverse Legit?

Yes. It publicly lists licensing, NMLS information, contact channels, and product disclosures. (Finance of America)

Who Owns Finance of America Reverse?

Public-facing pages identify the brand as a division of Finance of America Reverse LLC under the broader Finance of America identity. (Finance of America)

Is Finance of America Going Out of Business?

No current source reviewed here shows that Finance of America Reverse is going out of business. Current SEC-linked materials and lender pages indicate ongoing operations. (SEC)

How Long Does It Take to Receive Funds From Finance of America Reverse?

Funding time varies by appraisal, counseling, underwriting, and closing. In practice, reverse mortgages usually take weeks, not days. Finance of America’s public pages emphasize consultation and estimate steps rather than a guaranteed funding timeline. (Finance of America)

Are There Any Insurance Requirements?

Yes. Borrowers must maintain homeowners insurance, and HECMs involve FHA mortgage insurance. (HUD)

Can You Back Out of a Reverse Mortgage Contract?

Yes. FTC materials on reverse mortgages discuss the borrower’s right to cancel within the applicable rescission period after closing for eligible transactions. (Consumer Advice)

Reverse Mortgage Frequently Asked Questions

Can I Lose My Home With a Reverse Mortgage?

Yes. You can lose the home if you do not meet loan obligations such as property taxes, homeowners insurance, and required occupancy. (HUD)

What Happens If I Outlive the Equity From My Reverse Mortgage?

For a HECM, you may continue living in the home as long as you meet the loan terms, even if the balance grows significantly. (HUD)

Can I Still Leave My Home to My Kids With a Reverse Mortgage?

Yes. Heirs can sell the home, repay the balance, or refinance to keep it. They just inherit less net equity if the reverse mortgage balance is large.

How Does a Reverse Mortgage Impact Government Benefits Like Medicare and Social Security?

Reverse mortgage proceeds generally do not affect Medicare or Social Security benefits, but they can affect needs-based programs if funds are retained in ways that count as assets. Borrowers should confirm with a qualified benefits adviser before closing. (Consumer Advice)

Are Reverse Mortgages Government-Insured?

HECMs are government-insured through the FHA. Proprietary reverse mortgages such as HomeSafe are not FHA-insured. (HUD)

How We Evaluated Finance of America Reverse Mortgages

This review weighs 6 factors: product range, transparency, accessibility, regulatory and licensing signals, customer-service structure, and public credibility markers such as SEC activity, BBB presence, and official product disclosures. I also ignored irrelevant search noise that can appear around unrelated terms such as World Cup, Xponential Fitness, Modal title, NAF Promise, CFG, Work with Us, Parents, Real Estate Agents, Credit, Loans, Debt, and Consumer Alerts unless those terms clearly tied back to reverse mortgage lender information in the source set. (SEC)

Summary of Money’s Finance of America Reverse Mortgage Review

I did not find a current Money review page specifically for Finance of America Reverse in the returned results. I did find Money’s mortgage-review format for other lenders, which shows the kind of factors Money usually examines: pros and cons, pricing, offerings, accessibility, customer experience, and customer satisfaction. That framework fits this review well, but I am not claiming a current Money page for Finance of America Reverse without a direct source.