Key Takeaways

- Invoice financing for small business helps convert unpaid invoices into immediate cash to improve cash flow.

- Businesses receive an advance payment based on invoice value, then settle after customer payment is received.

- Options include invoice factoring, invoice discounting, selective financing, and spot factoring.

- Approval depends more on customer creditworthiness than the business’s own credit score.

- It is a flexible funding solution that supports growth without giving up equity or taking traditional loans.

Introduction

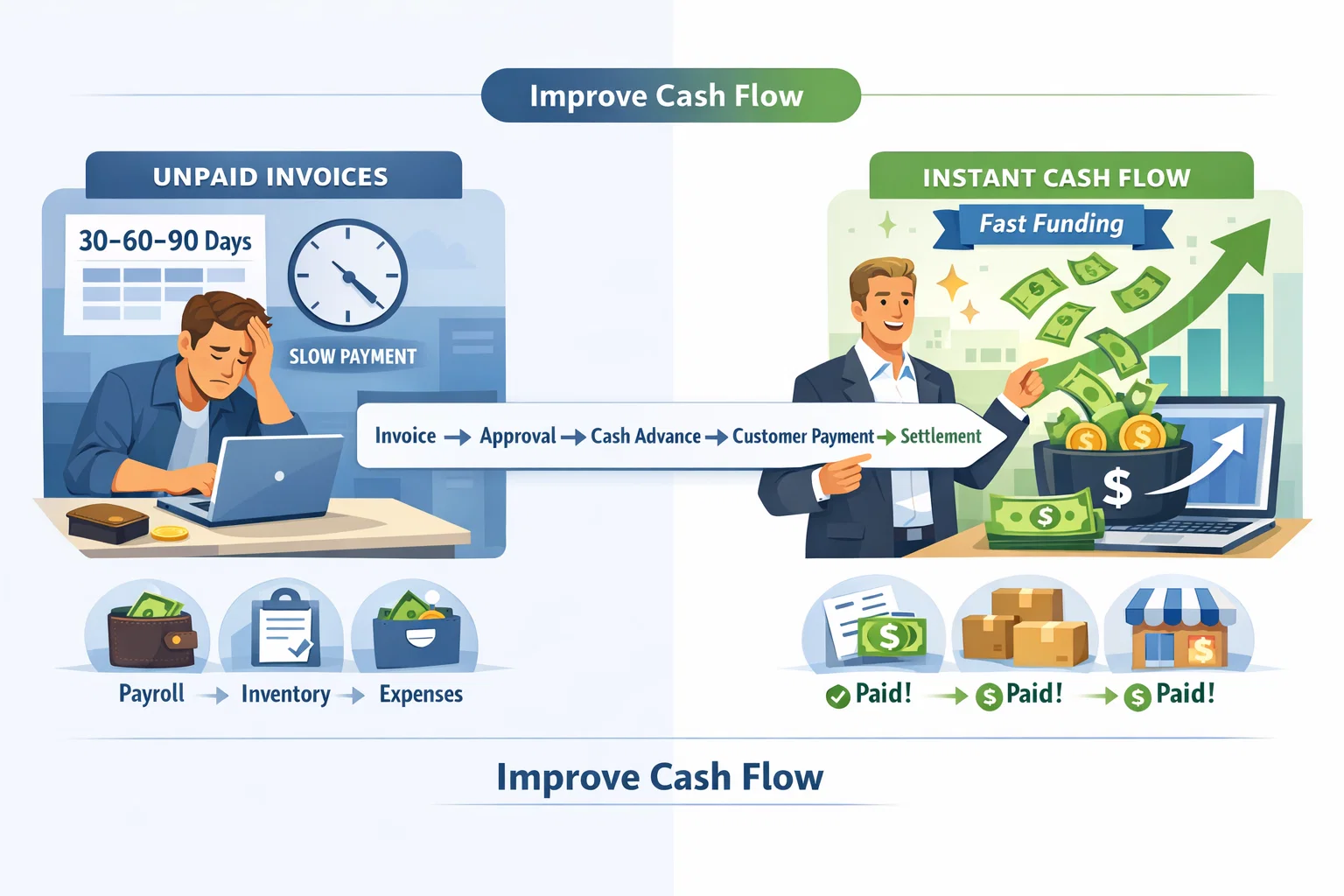

Invoice financing for small business is a funding method that lets a company unlock cash from unpaid customer invoices instead of waiting 30, 60, or 90 days to get paid. It works by using approved invoices as the basis for funding, which helps improve cash flow, cover payroll, buy inventory, and handle day-to-day operating costs without taking on a standard term loan.

The main parts of invoice financing are invoice submission, assessment, advance payment, customer payment, and settlement.

What is Invoice Financing?

Invoice financing is a form of accounts receivable financing that gives a business access to cash based on unpaid invoices. Instead of waiting for customers to pay, the business receives an advance from a financing provider. When the customer pays the invoice, the provider deducts its fees and sends the remaining balance to the business.

How Does Invoice Financing Work?

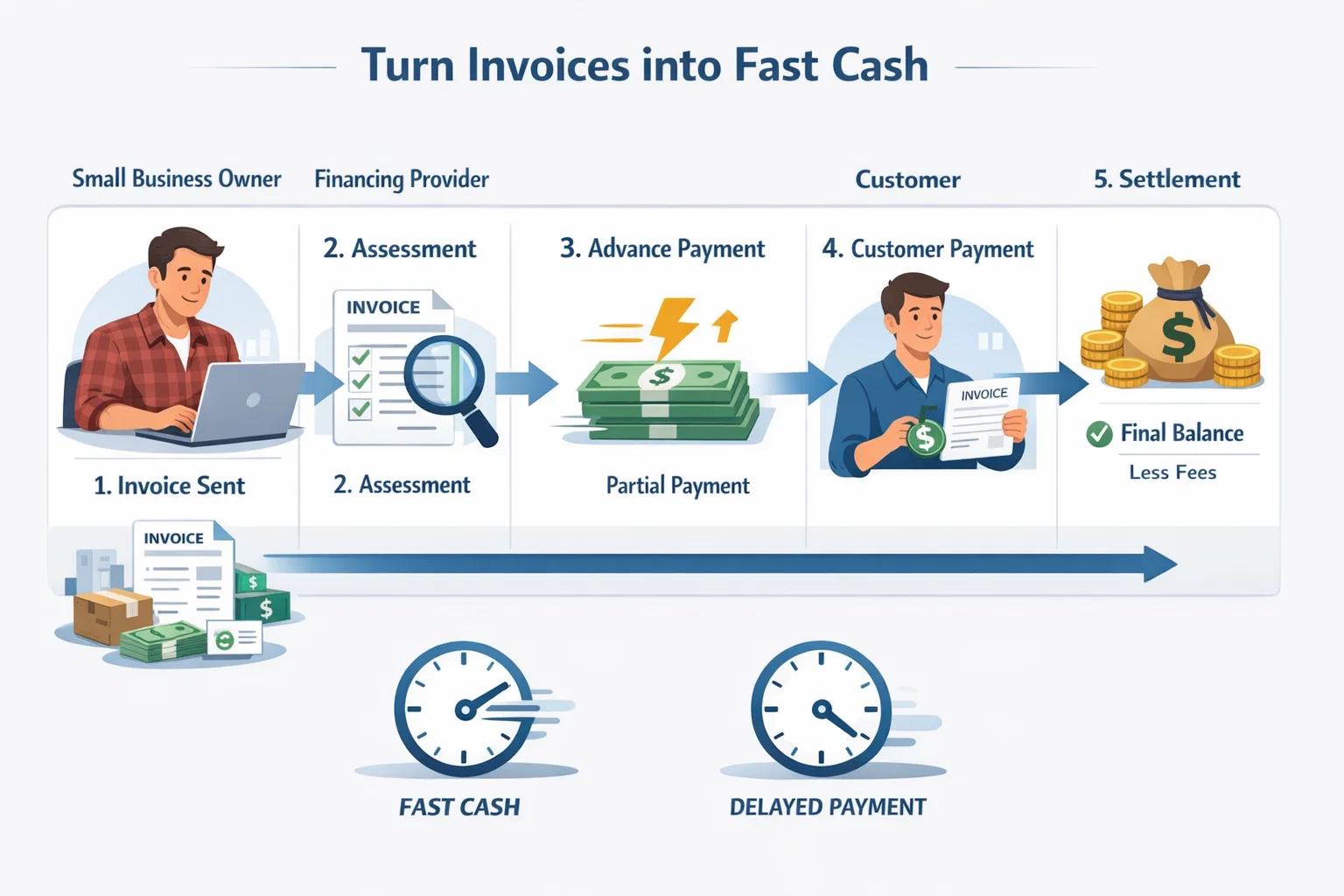

Invoice financing usually follows 5 steps: Invoice Submission, Assessment, Advance Payment, Customer Payment, and Settlement. The process is direct, and the goal is simple: turn unpaid invoices into faster cash.

Invoice Submission

The business sends one invoice or a batch of invoices to the financing company. These invoices usually come from completed work or delivered goods. The provider checks whether the invoices are valid, whether the customers are creditworthy, and whether the invoice terms fit its program.

Assessment

During Assessment, the financing provider reviews the invoice details, customer payment history, business structure, and risk level. The provider may ask for proof of delivery, purchase orders, signed contracts, and customer account history. A provider may look at Business Incorporation, Operational History, Annual Revenue, Invoice Value, and Invoice Terms before approving funding.

Advance Payment

After approval, the provider sends an Advance Payment. This is usually a percentage of the invoice amount, not the full value. The advance gives the business quick working capital to manage payroll, purchase stock, pay vendors, or cover operating costs.

Customer Payment

The customer makes Customer Payment according to the invoice terms. In some structures, the customer pays the financing company directly. In other structures, the customer continues paying the business, and the financing stays confidential.

Settlement

After payment is received, the provider completes Settlement. The provider deducts fees and releases the remaining amount to the business. This final amount is often called the reserve balance or remainder.

You Can Also Read Why Lenders Require Full Coverage Insurance On A Financed Car Explained

Types of Invoice Financing

There are several types of invoice financing. Each one fits a different business model, customer relationship, and cash flow need.

Invoice Factoring (Invoice Funding)

Invoice Factoring is a structure where the provider advances cash and usually takes over collection on the financed invoices. It is often called Invoice Funding. The provider may communicate directly with the customer, which means the customer usually knows the invoice has been factored.

Invoice factoring works well for companies that want a simple outsourcing model for receivables management. It is common in transportation, staffing, wholesale, and manufacturing. A Logistics Company waiting on Broker Payments or a Staffing Agency trying to meet Weekly Payroll often uses factoring because fast cash matters more than keeping collections in-house.

Invoice Discounting (Confidential Invoice Financing)

Invoice Discounting is often called Confidential Invoice Financing. The business still receives an advance against unpaid invoices, but it usually keeps control of customer collections. The customer may not know financing is being used.

This model fits businesses that want faster cash while protecting their existing customer relationships. It can work well for a B2B Service Company that wants to keep billing and collections under its own brand.

Selective Invoice Financing

Selective Invoice Financing allows the business to choose specific invoices instead of financing the whole ledger. This gives more control and can reduce unnecessary fees. A company may use this when only certain customers pay slowly or when only one part of the business needs temporary liquidity.

Spot Factoring

Spot Factoring is a one-off or occasional funding arrangement. Instead of signing up for continuous invoice funding, the business factors a single invoice or a small set of invoices. This can help during seasonal cash shortages, large one-time orders, or sudden operating expenses.

Ledgered Lines of Credit

Ledgered Lines of Credit are revolving facilities tied to accounts receivable. Instead of funding one invoice at a time, the provider gives access to a line based on the business’s ledger. This can offer more flexibility for growing companies that send invoices regularly and need repeated access to working capital.

Key Benefits of Invoice Financing

Invoice financing has several strong advantages for small businesses that deal with delayed customer payments.

Improved Cash Flow and Business Stability

The biggest benefit is better Cash Flow. A small business does not need to wait weeks or months for payment before using money it has already earned. This supports payroll, inventory purchases, supplier payments, rent, and daily operations. Better cash flow improves business stability and reduces the risk of late payments to employees or vendors.

Flexibility

Invoice financing is flexible because funding can rise or fall with actual invoice volume. A business can use it during busy periods, growth stages, or short-term slowdowns. This flexibility makes it different from a fixed loan with a fixed payment structure.

No Collateral Needed

Many invoice financing products do not require heavy hard-asset collateral. The invoice itself becomes the main funding basis. That can help small businesses that do not own equipment, property, or other assets that lenders normally want.

Credit Based on Customers

A major strength of invoice financing is that approvals often depend more on the credit quality of the customer than on the business owner’s personal credit. This is why invoice financing can help companies that have good customers but weak balance sheets or limited borrowing history.

Seize Growth and Expansion Opportunities

Fast access to receivables can help a company accept larger orders, hire staff, buy raw materials, expand into new markets, or handle new clients without waiting for old invoices to clear. That turns invoice financing into invoice-backed growth capital.

Debt-Free Financial Tool

Invoice financing is often described as a debt-free financial tool because it is based on receivables rather than a standard lump-sum loan. The business is unlocking money already tied to delivered work. It still has costs, but the structure is different from ordinary borrowing.

Scales with Your Sales

The more eligible invoices the business generates, the more funding capacity it may access. This makes invoice financing a strong fit for companies with growing sales and growing receivables.

Preserves Equity and Assets

Invoice financing does not dilute ownership. A company does not need to sell equity to raise short-term working capital. That helps preserve both ownership and asset flexibility.

Invoice Factoring vs. Invoice Discounting

Invoice factoring and invoice discounting both turn invoices into faster cash, but they work differently.

Feature Comparison

Invoice factoring usually includes direct involvement by the provider in collections. The customer often knows the invoice has been sold or assigned. Invoice discounting usually keeps collections with the business, so the financing may stay confidential.

Factoring is usually easier for smaller businesses that want simpler administration. Discounting often suits larger or more established companies that want to keep the customer relationship fully under their own control. Factoring may be more visible. Discounting may demand stronger internal billing systems and stronger financial controls.

Who is Invoice Financing Best For?

Invoice financing is best for businesses that sell to other businesses or institutions on payment terms. It works especially well for companies that face delayed collections but must pay expenses now.

This often includes:

- a Manufacturing Company facing long payment cycles

- a Logistics Company waiting for broker payments

- a Staffing Agency covering weekly payroll

- a B2B Service Company handling growth

- eCommerce businesses selling through wholesale or business channels

- agencies, wholesalers, and contractors with approved receivables

A business that is paid instantly by consumers usually gains less from invoice financing than a business that bills large customers on net terms.

Criteria for Obtaining Invoice Financing

Providers look for a mix of business quality, customer quality, and invoice quality.

Business Incorporation

Most providers prefer a formally registered business. Business Incorporation helps confirm the company’s legal structure, ownership, and operating status.

Operational History

Operational History matters because providers want to see that the company has real customers, completed work, and an ongoing invoicing pattern. A longer track record may improve approval odds, but some providers can still work with younger businesses.

Annual Revenue

Annual Revenue gives providers a sense of business scale. The exact amount required varies, but steady revenue helps show the business can keep producing invoices.

Invoice Value

The size of the Invoice Value matters. Providers may have minimum or maximum invoice thresholds, and larger approved invoices often create stronger funding opportunities.

Invoice Terms

Invoice Terms matter because providers prefer clear due dates, commercial customers, and verifiable payment conditions. Shorter and cleaner invoice terms are usually easier to finance than complex or disputed invoices.

Step-by-Step Guide to Using Invoice Financing

A business can use invoice financing more effectively by following a simple process.

Assess Your Cash Flow Needs

Start by identifying why cash is tight. The problem may be payroll timing, supplier terms, growth, seasonal demand, or delayed payments from a few major customers. Once the business knows the exact need, it can choose the right invoice financing structure.

Choose the Right Invoice Financing Provider

Compare providers on advance rate, fee structure, customer communication, funding speed, minimum volume, contract flexibility, and industry fit. Some providers specialize in Freight Factoring, some focus on trade finance, and some work broadly across service industries.

Submit Invoices and Access Funds

Once approved, submit eligible invoices and request funding. This is where Invoice Submission becomes the trigger for faster cash. The business receives funds, usually as an advance against approved invoices.

Manage Repayments and Monitor Cash Flow

After customer payments come in, monitor settlements, fees, reserves, and outstanding receivables. A business should treat invoice financing as a cash flow management tool, not as a reason to ignore collections discipline.

Comparisons

Invoice financing should be compared with other funding tools before making a decision.

Invoice Financing vs. Business Loans

A business loan usually depends more on business credit, personal guarantees, financial statements, and debt capacity. Invoice financing depends more on receivables. A loan gives one lump sum. Invoice financing moves with invoice flow.

Invoice Financing vs. Lines of Credit

A line of credit gives flexible borrowing up to a set limit, but approval often depends on stronger credit and underwriting. Invoice financing may be easier for businesses with weak credit but strong customers.

Invoice Financing vs. Merchant Cash Advances

Merchant cash advances are usually tied to future sales and can be expensive. Invoice financing is usually more structured and directly tied to completed work and issued invoices. For B2B companies, invoice financing is often more predictable.

Invoice Financing vs. Waiting for Customer Payment

Waiting for payment costs no financing fee, but it can create cash gaps, delay payroll, limit inventory, and block growth. Invoice financing costs money, but it can reduce business disruption and help the company keep moving.

Best Practices and Tips for Using Invoice Financing

A smart business uses invoice financing carefully and with a clear plan.

When to Use Invoice Financing

Use invoice financing when invoices are valid, customers are reliable, and the business needs short-term working capital for clear reasons. It works well during growth, seasonal demand, long receivable cycles, and temporary liquidity pressure.

Understanding Costs and Fees

A business should understand advance rates, discount fees, service charges, late-payment risks, and any extra administrative fees. The lowest advertised rate may not be the cheapest real option once all charges are added.

Connecting Financing with eCommerce Platforms

Some modern providers work with eCommerce and digital systems. Businesses using Shopify, Amazon, or similar channels may benefit when funding tools connect with invoicing, accounting, or payment systems. That can reduce manual work and improve visibility.

Practical Examples or Scenarios

A Manufacturing Company Facing Long Payment Cycles

A Manufacturing Company ships large orders to distributors with 60-day payment terms. Raw materials and labor must be paid now. Invoice financing helps turn those invoices into immediate working capital so production continues without delay.

A Logistics Company Waiting for Broker Payments

A Logistics Company delivers loads but waits weeks for Broker Payments. Fuel, repairs, and driver expenses continue daily. Freight-style invoice financing helps keep trucks moving.

A Staffing Agency Meeting Weekly Payroll

A Staffing Agency may invoice clients monthly but must pay workers every week. That mismatch is a classic reason to use invoice financing. The agency can cover Weekly Payroll without waiting for client payments.

A B2B Service Company Responding to Growth

A B2B Service Company wins a larger client and must hire staff quickly. Receivables look strong, but cash is tight. Invoice financing provides growth support without selling ownership or waiting for a bank loan.

Things to Consider for Invoice Financing

Invoice financing is useful, but it is not automatic or free.

Customer Types

The best invoices usually come from established commercial customers with a strong payment record. A provider may be less interested in invoices from new, unstable, or hard-to-verify buyers.

Customer Relationships

Some businesses care deeply about how customers are contacted. If confidentiality matters, invoice discounting may be a better fit than factoring.

Costs

The main cost question is simple: does the faster cash produce more value than the financing fee? If the answer is yes, the tool may make sense. If the margins are too thin, it may not.

Pros and Cons of Invoice Financing

Advantages

Invoice financing improves cash flow, supports growth, preserves equity, reduces pressure from long payment terms, and often avoids heavy collateral requirements. It can be faster than traditional lending and can scale with invoice volume.

Disadvantages

Invoice financing can cost more than some bank products. Customer quality matters. Not every invoice qualifies. Some arrangements may affect customer communication. If customers pay late, the business may face higher costs or delayed settlement.

Common Use Cases of Invoice Financing

Common use cases include payroll support, inventory purchases, vendor payments, seasonal demand, freight operations, staffing costs, manufacturing orders, trade finance, and short-term cash flow gaps. It is especially common where companies do real work now but get paid later.

How to Qualify for Invoice Financing?

To qualify, a business usually needs valid unpaid invoices, commercial customers, clear payment terms, completed delivery or service, and documentation that proves the receivable is real. Some providers also want minimum revenue, operating history, and clean business records.

How to Apply for Invoice Financing?

A business usually applies by submitting company details, customer information, sample invoices, accounts receivable aging, bank statements, and formation documents. The provider reviews the file, approves eligible customers and invoices, and sets the advance structure. After that, funding can begin with approved invoice submission.

How Much Does Invoice Financing Cost?

Invoice financing cost depends on advance rate, invoice term, customer risk, industry, provider structure, and whether the arrangement is ongoing or selective. The business should look at the total fee, not only the advertised rate. It should also ask whether the provider charges setup fees, wire fees, lockbox fees, or minimum usage fees.

Invoice Financing in India

In India, invoice financing may involve local documentation, tax treatment, and business records such as GST Invoice Bill support, electronic invoicing processes, and local compliance requirements. Businesses should review how invoice finance fits into their Financial System, billing method, and payment structure before applying.

Automation Options in Invoice Financing

Automation is becoming more important in invoice financing. Providers and businesses can automate invoice upload, customer verification, payment tracking, reserve reconciliation, and reporting. Artificial Intelligence can support risk review, fraud detection, payment trend analysis, and invoice matching. Businesses using digital accounting, Electronic Payment workflows, and integrated billing tools can reduce manual errors and speed up funding decisions.

Summary

Invoice financing for small business is a practical way to turn unpaid invoices into faster working capital. It helps improve cash flow, support payroll, fund inventory, and handle growth without waiting for slow-paying customers. The core process stays the same: invoice submission, assessment, advance payment, customer payment, and settlement. The best fit is usually a business with reliable B2B invoices, clear payment terms, and a real need for faster cash. Used well, invoice financing can become a flexible funding tool that grows with sales, protects equity, and gives a small business more control over its cash flow.

FAQs

How to Get Invoice Financing?

Start by identifying eligible unpaid invoices, then compare providers, submit business and customer documents, and request funding against approved receivables.

Is Invoice Financing Easy to Get?

It can be easier to get than a traditional business loan if the business has strong customers and valid invoices. Approval often depends more on receivables quality than on hard collateral.

Can I Use Invoice Financing if I Have Bad Credit?

Yes, in many cases. A provider may still approve funding if the customer paying the invoice has strong credit and the receivable is valid.

How Fast Can I Receive Funds?

Funding speed varies by provider and documentation quality. Once the account is set up, approved invoices can often be funded much faster than a standard loan process.

Does Invoice Financing Affect Customer Relationships?

It can, depending on the structure. Factoring may be visible to customers. Discounting may remain confidential. Businesses that care about customer contact should ask about collections and notice procedures.