Key Takeaways

- Yes, roofing companies that finance can be a good option if you need a roof now and cannot pay the full cost upfront.

- Roof financing options include personal loans, HELOCs, credit cards, government-backed programs, PACE financing, and roofing company payment plans.

- The best financing plan depends on your credit, home equity, project cost, and how fast the roof work must be done.

- Homeowners should compare APR, monthly payments, total repayment cost, fees, and lender terms before signing any financing agreement.

- Roofing financing helps protect your home quickly, but bad terms or scam offers can make the project much more expensive over time.

Introduction

Roofing companies that finance help homeowners spread roof replacement or roof repair costs over time through payment plans, personal-loan partners, home-equity products, or specialized consumer financing. That matters when a roof leak, storm loss, or aging roof cannot wait for months of savings. The main benefits are faster project approval, lower upfront cash pressure, and access to a new roof when the home needs it now.

Understanding Roof Replacement Costs

A roof replacement cost depends on material, labor, roof complexity, and the amount of repair work hidden under the shingles. Homeowners usually finance a roof when the total price is too large for cash payment or when keeping cash reserves matters more than paying in full. HUD notes that home-improvement financing can cover both labor and materials, which is why roof financing is often used for full replacements and not only small repairs. (HUD)

Factors Influencing Costs

There are 4 main cost drivers: roofing materials, labor costs, roof size and design, and the choice between repair and replacement. A simple asphalt shingle roof costs less than a concrete tile roof, metal roof, or roof with solar shingles. A steep roof, a cut-up roofline, or a home with several valleys and penetrations raises labor time and safety requirements. (HUD)

Roofing Materials

Roofing materials change the total budget fast. Asphalt shingles usually cost less than metal, tile, or premium designer shingles from brands such as Malarkey, Atlas, GAF, Owens Corning, or CertainTeed. Material choice affects lifespan, appearance, wind resistance, and how much a lender or roofing contractor may suggest financing.

Labor Costs

Labor costs rise when the tear-off is harder, access is limited, or the crew must work around chimneys, skylights, solar panels, or multi-story layouts. Local labor markets in places such as Illinois, Naperville, IL, Raleigh, NC, Florida, California, or Pennsylvania can shift pricing too. A homeowner should always ask how much of the quote is labor and how much is material.

Roof Size and Design

A larger roof needs more shingles, underlayment, flashing, and installation time. Complex roof design adds waste, more cuts, and more safety setup. That is why two homes with the same square footage can have very different roof financing needs.

Repair vs. Replacement

A repair can cost less today, but a full replacement can cost less over the next 10 to 20 years if the roof is already near the end of its service life. Financing a replacement often makes more sense than financing repeated emergency roof repairs on an old roof.

Additional Costs

Beyond the main quote, homeowners should expect extra line items for decking repairs, permit fees, disposal, upgraded ventilation, flashing replacement, gutter work, and insurance-related documentation. Those extras can make a low initial estimate look much less attractive once the contract is final. (HUD)

Necessary Materials

Necessary materials include underlayment, drip edge, flashing, vents, fasteners, starter strips, ridge caps, ice-and-water protection where needed, and disposal supplies. These items are not minor add-ons. They are part of a proper roof installation.

Special Features

Special features raise cost and financing needs. Skylights, solar panels, gutter guards, premium ventilation systems, impact-rated shingles, designer roofing shingle systems, and steep-slope ladder safety requirements all add to the project total.

Why Finance Your Roof?

Finance your roof when the work is urgent, the cash cost is high, or preserving savings matters more than paying the full project price today. Roof financing can prevent interior water damage, mold growth, insulation damage, and structural decay that often cost more than the financing itself. Financing can be useful for storm damage claims too, especially when insurance covers part of the job but leaves a deductible or upgrade gap. (HUD)

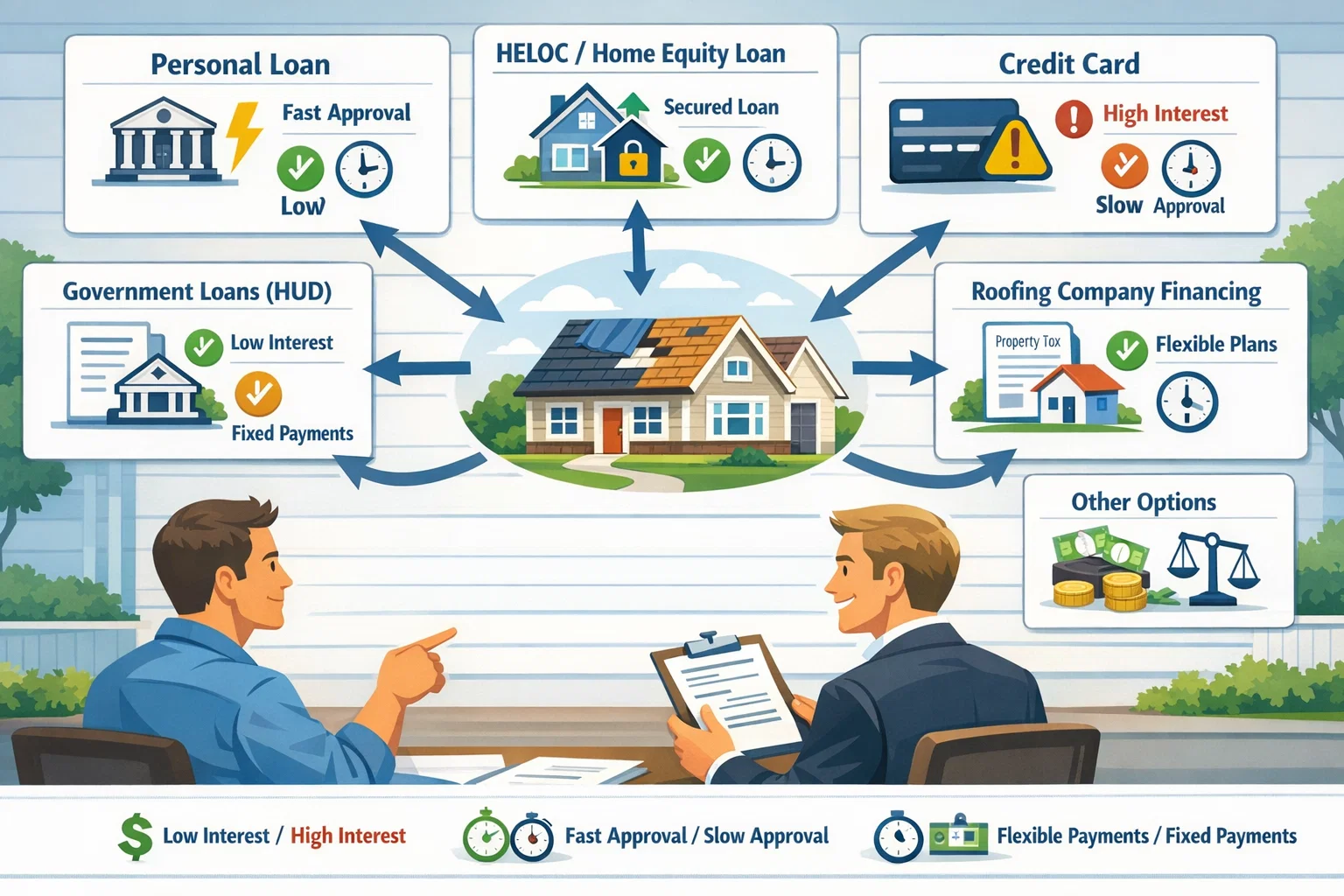

Roof Financing Options Explained

There are 7 common roof financing options: personal loans, home equity loans or HELOC products, credit cards, government-backed programs, roofing company financing, PACE financing, and HUD home-improvement loans. The right choice depends on credit profile, project urgency, available equity, and how long you want to repay the debt. (HUD)

YOU CAN ALSO RAED How Finance Of America Reverse Works For Homeowners Seeking Reverse Mortgage Options

Common Financing Options

Personal Loans

Personal loans are unsecured loans offered by banks, credit unions, and online lenders. They usually fund faster than home-equity products and do not require home equity. That makes them useful for emergency roof financing. The tradeoff is that APR can be higher than secured options, especially for bad-credit applicants.

Home Equity Loans (HELOC)

A Home Equity Loan or Home Equity Line of Credit (HELOC) uses home equity as collateral. These products often offer lower rates than unsecured personal loans, but closing can take longer and the home is part of the risk profile. A HELOC can work well when the roof project is planned and the homeowner wants flexible draws. A standard home equity loan fits homeowners who want one set borrowing amount and one repayment schedule.

Credit Cards

Credit cards can work for small roof repairs or deductibles, but credit cards are usually the most expensive way to finance a full roof replacement if the balance is not paid quickly. A 0% introductory offer can help in limited cases, but most roof projects are too large for long-term card use.

Government Loans and Programs

Government-supported financing can include HUD improvement products and local or state repair programs. HUD says Title I Property Improvement Loans can be used for improvements that protect or improve basic livability or utility, and HUD’s home-improvement pages explain that insured loans may cover both labor and materials. Those details make Title I relevant for some roofing projects. (HUD)

Roofing Company Financing/Payment Plans

Roofing Company Financing is one of the most common paths for homeowners. The contractor partners with one lender or several lenders and lets the customer apply at the point of sale. Platforms such as Wisetack market fast approval, monthly payment options, and eligibility checks that do not impact credit score during prequalification, while BuyFin markets multi-lender decisioning and mobile-first contractor tools. This is why many homeowners search for roofing companies that offer financing or roofing contractors that finance. (wisetack.com)

PACE Financing

PACE Financing is repaid through a property-tax assessment rather than a standard monthly installment loan. CFPB explains that a PACE loan increases your property tax payment and warns borrowers to compare alternatives before signing. PACE can be attractive for high-cost improvements with no down payment, but CFPB also warns about fees, interest, and home-risk concerns if the obligation becomes unaffordable. (Consumer Financial Protection Bureau)

HUD Home Improvement and Repair Loan

A HUD Home Improvement and Repair Loan usually refers to HUD-insured Title I financing for repairs and improvements, and in some situations homeowners may look at FHA 203(k) refinancing if the roof work is tied to a purchase or refinance. HUD says Limited 203(k) can finance up to $75,000 in repairs or upgrades rolled into a mortgage. That makes it more useful for broader renovation plans than for a simple roof-only project in many cases. (HUD)

Choosing the Right Financing Option

Choose the right financing option by comparing 5 things: total project cost, total borrowing cost, approval speed, collateral risk, and payment flexibility. A homeowner with strong equity may prefer a HELOC. A homeowner with an urgent leak may prefer contractor financing or a personal loan. A homeowner considering PACE should compare the property-tax impact against every other option first. (Consumer Financial Protection Bureau)

Pros and Cons of Financing a Roof Replacement

Financing a roof replacement can be smart, but only when the payment terms are clear and affordable. The biggest benefit is that it lets the homeowner solve a real housing problem now. The biggest risk is paying too much for that speed. (HUD)

Pros

Low Monthly Payments

Low monthly payments make a full roof replacement easier to manage than one large cash bill. Many roofing finance offers succeed because homeowners think in monthly affordability, not just total price.

Defer/Delay Payments

Some programs offer deferred or delayed payments. That can help after a storm loss or during a temporary cash crunch, but deferred interest terms need careful review before signing.

Quick Approval Process

A quick approval process matters in roofing. Wisetack says some applicants can see options in under a minute, and contractor-financing platforms often promote mobile-first approvals in the field. Fast decisions help close urgent roof repairs before more damage develops. (wisetack.com)

Cons

The main cons are higher total cost, possible fees, pressure-selling risk, and contract complexity. Financing can make an overpriced roofing project look affordable by shrinking the monthly number while hiding the true total paid over time. Secured products can put the home at greater risk. PACE adds property-tax repayment complexity. Poorly explained contractor financing can trap a homeowner in expensive debt. (Consumer Financial Protection Bureau)

Is Financing a Roof Replacement a Good Idea?

Yes, financing a roof replacement is a good idea when the roof work is necessary, the payment fits your budget, and the financing terms are competitive. It is a bad idea when the roof can wait, the APR is too high, or the financing contract is unclear. The answer is not about financing alone. The answer is about whether the financing solves a real problem at a manageable cost.

Situations Where Financing Makes Sense

Financing makes sense when the roof is leaking, the insurer is paying only part of the claim, the home must be protected quickly, or savings need to stay available for emergency reserves. It can make sense for energy upgrades too, including better ventilation or some solar-related roof work.

When Paying in Full Might Be Better

Paying in full is usually better when you have enough cash, the financing APR is high, the project is small, or the lender requires risky terms. Cash can strengthen price negotiation with a roofing company and avoids interest altogether.

What to Look for in a Roofing Financing Plan

Look for 8 details: APR, fees, prepayment penalties, length of repayment, deferred-interest rules, credit-check method, lender identity, and what happens if the project changes after tear-off. A good Roofing Financing Plan should show the full amount financed, the total of payments, and whether the contractor gets paid before or after completion.

Roof Financing Options for Homeowners with Bad Credit

Homeowners with bad credit usually have fewer low-rate options, but they still may qualify through contractor-financing platforms, secured home-equity products, co-borrowers, or lenders with wider approval ranges. BuyFin markets multi-lender coverage and says broader approval can help contractors serve more customer profiles, while contractor platforms in general often approve more applicants than a single bank offer. Bad-credit homeowners should be extra careful with no-credit-check claims. Those offers often come with very high cost or risky contract terms. (BuyFin)

How to Qualify for Roof Financing

Qualification usually depends on credit score, debt-to-income ratio, income stability, project size, and in some cases home equity. For contractor financing, prequalification may be soft-pull only. For HELOC and home-equity loans, the lender will usually review income, property value, and lien position more deeply. Government-backed products can have extra property and documentation rules. (HUD)

Tips for Choosing the Right Roof Financing Plan

Compare at least 3 financing paths before signing. Ask for both monthly payment and total repayment amount. Check whether the rate is fixed or promotional. Ask whether there is a penalty for early payoff. Confirm whether the financing is from the roofing contractor, a bank, or a third-party platform. Good financing is clear. Bad financing depends on hurry and confusion.

What to Do Before Applying for Financing

Do the roof homework first. A rushed financing decision often starts with a rushed roofing quote.

Conduct a Roof Inspection

Get a real roof inspection before applying. The goal is to confirm whether you need repair, partial replacement, or full replacement. A roof inspection can also help with Roofing Insurance claims and deductible planning.

Gathering Multiple Estimates

Gather multiple estimates from at least 2 to 4 roofing companies. HUD’s consumer guidance on home improvements says to get more than one estimate and to read and understand what you sign. That advice applies directly to roof replacement financing. (HUD)

Setting a Budget

Set a budget that includes the monthly payment, not only the total quote. Include deductible amounts, ventilation upgrades, decking repair allowances, and a cash reserve for surprises.

Negotiating Terms

Negotiate the project terms and the financing terms separately. A contractor may be flexible on labor, upgrade pricing, or payment timing. A financing partner may be flexible on term length or lender match, but not necessarily on rate.

Spotting Red Flags and Avoiding Scams

Roofing scams and financing scams often show up together after storms, when urgency is high and homeowners are stressed. HUD’s home-improvement pages warn that deceptive contractors have falsified documents, overcharged homeowners, and performed poor work in government-related repair settings. That warning applies far beyond government programs. (HUD)

Common Red Flags in Finance Agreements

Common red flags include blank spaces in contracts, pressure to sign the same day, unclear APR, deferred-interest language buried in fine print, huge dealer fees, no cancellation explanation, no lender name, and promises of guaranteed approval. Another red flag is when a salesperson focuses only on monthly payment and refuses to discuss total repayment.

Tips for Avoiding Untrustworthy Lenders

Read the full financing disclosure. Confirm the legal lender name. Compare outside offers. Do not sign because a sales rep says the offer is “today only.” Be careful with “no credit roof” or “roof now, pay later” claims that sound easier than the paperwork shows. If the financing is through PACE, read the property-tax repayment details line by line. (Consumer Financial Protection Bureau)

Summary

Roofing companies that finance help homeowners replace or repair a roof without paying the full amount at once. The article explains roof costs, common financing options, and how insurance and financing can work together. It also covers how to compare loan terms, avoid scams, and choose a payment plan that fits your budget. A good financing plan can make a new roof easier to afford while protecting your home from bigger damage.

FAQs

1. Do roofing companies offer financing?

Yes, many roofing companies offer financing through partner lenders or payment plan providers.

2. Can I finance a roof replacement with bad credit?

Yes, some lenders and roofing companies offer options for bad-credit borrowers, though rates may be higher.

3. What is the best way to finance a new roof?

The best option depends on your budget, credit score, home equity, and how quickly you need the work done.

4. Can insurance and roof financing be used together?

Yes, insurance may cover part of the cost, while financing can help pay the deductible or uncovered upgrades.

5. What should I check before signing a roofing financing plan?

Check the APR, monthly payment, total repayment amount, fees, lender name, and any prepayment penalties.