Key Takeaways

-

Mandatory Minimums: Florida drivers must currently carry $10,000 in Personal Injury Protection (PIP) and $10,000 in Property Damage Liability (PDL) to drive legally.

-

The 14-Day Rule: You must seek medical treatment within 14 days (336 hours) of a car accident to qualify for PIP benefits, or your claim will be denied.

-

No-Fault System: Florida’s no-fault law means your own insurance pays for your injuries first, covering 80% of medical bills and 60% of lost wages regardless of who caused the crash.

-

2026 Policy Shifts: Legislation for 2026 aims to repeal PIP and replace it with mandatory Bodily Injury Liability (BIL) of $25,000 per person and $50,000 per accident.

-

Secondary Health Coverage: Humana health insurance acts as secondary coverage in Florida, paying for medical costs only after your PIP benefits are fully exhausted

Introduction

Humana health care insurance is a comprehensive medical coverage system where members pay premiums to access a structured network of doctors, hospitals, and pharmacies.

There are 3 main benefits of Humana health care insurance: access to a vast provider network, integrated wellness programs like HumanaVitality, and specialized Medicare Advantage (MA) plans.

Members use Humana health insurance to cover routine checkups, manage chronic conditions, and reduce the cost of prescription drugs.

Florida Car Insurance: Requirements, Coverage, and Changes

Florida Auto Insurance Requirements

Florida law requires every driver to carry specific types of auto insurance to maintain a valid vehicle registration. These rules ensure that drivers have immediate financial resources following a collision on state roads.

Legal Requirements to Drive in Florida

A Florida driver must maintain active insurance coverage to drive legally in the state. Driving without insurance results in the suspension of your driver’s license, vehicle tags, and registration for up to 3 years.

Mandatory Minimum Coverages in Florida

There are 2 mandatory minimum coverages in Florida: Personal Injury Protection (PIP) and Property Damage Liability (PDL). Every vehicle owner must carry $10,000 in PIP and $10,000 in PDL from an insurance company licensed in Florida.

Personal Injury Protection (PIP) Insurance

Personal Injury Protection (PIP) Insurance is a “no-fault” coverage that pays for medical expenses regardless of who caused the accident. This coverage ensures that Jacksonville drivers receive prompt medical attention without waiting for legal fault to be determined.

What PIP Covers

PIP covers 80% of necessary medical expenses and 60% of lost wages resulting from a car accident. Covered services include emergency room visits, dental work, rehabilitative services, and ambulance transportation.

PIP Coverage Benefits

There are 4 primary PIP coverage benefits, including immediate payment for medical bills, coverage for passengers who do not own a vehicle, protection for pedestrians, and a $5,000 death benefit.

Critical PIP Rules

Florida has strict regulations regarding how and when you can claim your PIP benefits. Failure to follow these rules results in a total loss of coverage for that specific incident.

The 14-Day Rule

The 14-Day Rule requires you to seek medical treatment within 14 days of an accident to qualify for PIP benefits. If you wait longer than 14 days (336 hours) to see a doctor, your insurance company will deny your claim entirely.

Property Damage Liability Insurance

Property Damage Liability (PDL) insurance pays for damage you or members of your household cause to another person’s property while driving. This includes damage to other cars, buildings, fences, or utility poles.

Liability Coverage

Liability coverage protects your personal assets if you are sued following a crash. While Florida only mandates PDL, many Jacksonville injury lawyers recommend adding Bodily Injury Liability (BIL) to your policy for complete protection.

Uninsured Motorist (UM) Coverage and Underinsured Motorist (UIM) Coverage

Uninsured Motorist (UM) coverage pays for your injuries if the at-fault driver has no insurance. Florida’s uninsured motorist rate is approximately 20%, making this optional coverage vital for North Florida drivers.

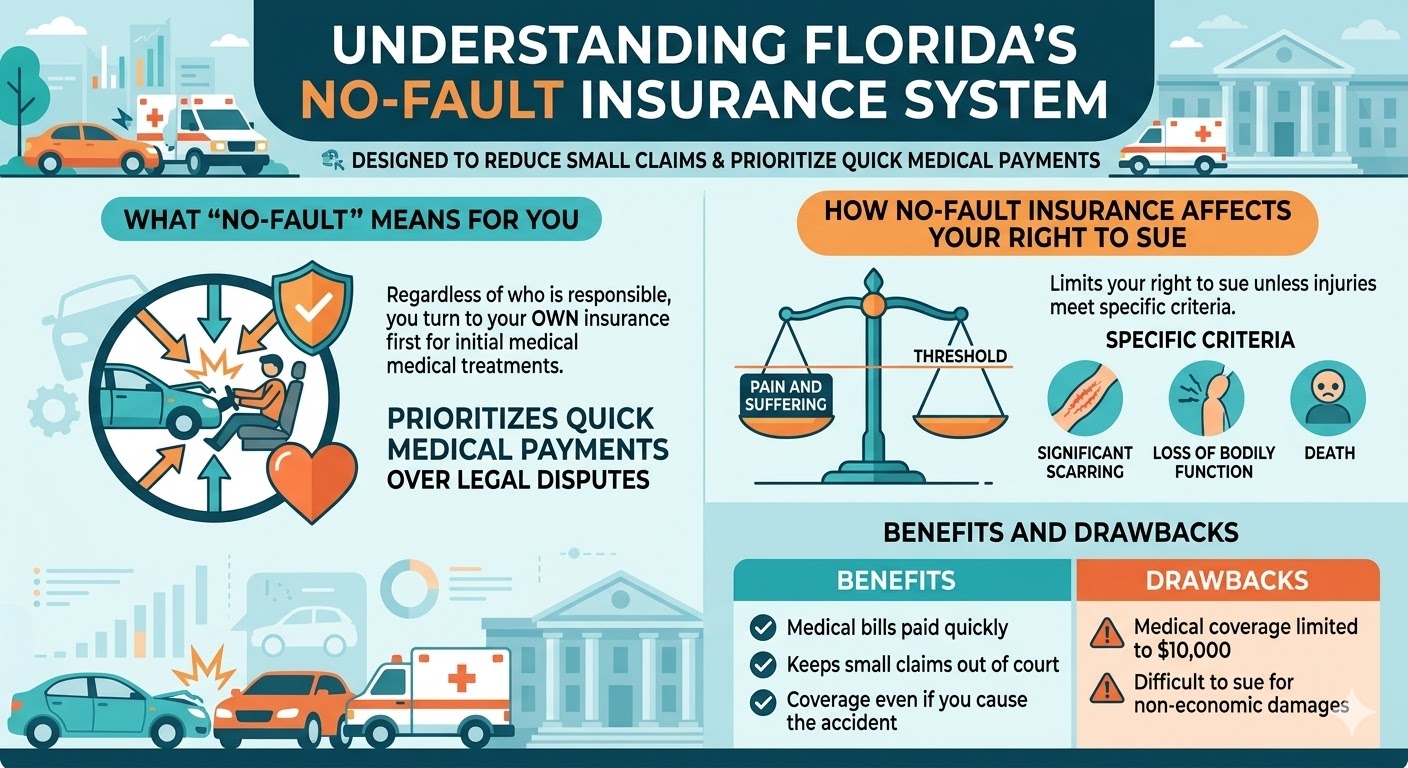

Understanding Florida’s No-Fault Insurance System

The no-fault system was designed to reduce the number of small claims in the court system. It prioritizes quick medical payments over legal disputes.

What “No-Fault” Means for You

No-fault means that your own insurance provider pays for your initial medical treatments regardless of who is responsible for the accident. You turn to your own PIP insurance first, even if the other driver was clearly at fault.

How No-Fault Insurance Affects Your Right to Sue

Florida law limits your right to sue for “pain and suffering” unless your injuries meet a specific threshold. This permanent injury threshold includes significant scarring, loss of a bodily function, or death.

The Benefits and Drawbacks of No-Fault Insurance

The no-fault system offers a mix of efficiency and limitations for drivers in Jacksonville, Florida.

Benefits

-

Medical bills are paid quickly.

-

Small claims are kept out of court.

-

Drivers are covered even if they cause the accident.

Drawbacks

-

Medical coverage is limited to $10,000.

-

Suing for non-economic damages is difficult.

-

Fraud in the PIP system often leads to higher premiums.

Common Challenges with Florida’s No-Fault System

High rates of insurance fraud and the $10,000 coverage limit, which has not changed since 1979, remain major challenges. Many Jacksonville car accident claims exceed this limit within hours of an emergency room visit.

Optional Coverages

While the state only requires two types of insurance, those minimums rarely provide enough protection for a serious accident in Downtown Jacksonville or Ponte Vedra Beach.

Optional Jacksonville Car Insurance

Jacksonville drivers often add extra layers of protection to avoid out-of-pocket expenses. Local agents at Shapiro Insurance Group or Lewis Insurance Agency can help customize these options.

Optional Coverage Options Include:

-

Bodily Injury Liability (BIL): Covers injuries you cause to others.

-

Collision Coverage: Pays for repairs to your own car.

-

Comprehensive Coverage: Covers theft, fire, and weather damage.

-

Medical Payments (MedPay): Covers the 20% gap left by PIP.

Car Insurance Changes for 2026: PIP Repeal

Significant Florida car insurance laws (2025) have set the stage for a transition in 2026. The Florida legislature has debated the PIP Repeal to move toward a mandatory bodily injury system.

What’s Changing

The 2026 changes involve replacing the $10,000 PIP requirement with a mandatory Bodily Injury Liability (BIL) requirement of at least $25,000 per person and $50,000 per accident.

Impact on Your Coverage

If the PIP repeal occurs, you will no longer receive 80% medical coverage from your own insurer by default. Instead, the at-fault driver’s insurance will be responsible for your medical bills and property damage.

Financial Impact of the Changes

Shifting from no-fault to a fault-based system will change how premiums are calculated for everyone in Florida.

Potential Savings

Some drivers may see potential savings of 5% to 10% on their total premium if fraud-heavy PIP costs are eliminated. However, the requirement to buy BIL coverage may increase costs for those currently only carrying the bare minimum.

What This Means for North Florida Drivers

North Florida drivers will need to rely more heavily on their health insurance for initial medical costs. Humana health insurance plans or other medical policies will become the primary source of payment for car accident injuries.

Preparing for the 2026 Transition

Transitioning to a new insurance law requires proactive steps to ensure you are never without legal coverage.

Review Your Current Coverage

Review your current policy document to see if you already carry Bodily Injury Liability. If you do not, you will need to add it before the 2026 deadline.

Consider Additional Protection

Purchase Uninsured Motorist (UM) coverage to protect yourself if the PIP safety net is removed. This ensures you have medical funds even if an at-fault driver flees the scene.

Shop Around for Coverage

Compare car insurance Jacksonville quotes from multiple providers like Mercury or Geico. Rates will fluctuate as companies adjust to the new 2026 regulations.

Factors Affecting Insurance Rates

Insurance companies use complex algorithms to determine your monthly premium.

Factors Influencing Auto Insurance Costs in Florida

There are 5 main factors influencing auto insurance costs in Florida: your driving record, credit-based insurance score, the age of the driver, the vehicle’s safety features, and your Jacksonville ZIP code.

How to Find the Best Auto Insurance

Finding the right policy requires more than just looking for the lowest price.

Steps to Find the Right Policy

-

Identify your specific coverage needs.

-

Gather quotes from at least 3 different companies.

-

Check the financial stability of the insurer.

-

Read Jacksonville insurance policy reviews.

Save More with Discounts

You can save more with discounts by bundling your personal insurance and business insurance. Ask about Florida teen driver insurance discounts or safe driver programs.

What Auto Insurance Doesn’t Cover

Auto insurance does not cover 4 specific scenarios: intentional damage, wear and tear, racing incidents, and use of the vehicle for commercial deliveries without a specific rider.

Common PIP Claims Process

The PIP claims process is designed to be straightforward so medical providers get paid.

Steps to File a Claim

-

Seek medical treatment within 14 days.

-

Notify your insurance company of the accident.

-

Provide the medical facility with your insurance information.

-

Submit any lost wage documentation to your adjuster.

Payment Timeline

Insurance companies must pay or deny a PIP claim within 30 days of receiving notice. If the claim is “red-flagged” for fraud investigation, the timeline may extend by an additional 60 days.

What to Do After an Accident with an Uninsured Driver?

Accidents involving uninsured drivers are common in Jacksonville.

Steps to Take After a Car Accident in Florida

-

Call the Florida Highway Patrol or local police to file a report.

-

Take photos of the damage and the other driver’s license.

-

Contact a Jacksonville car accident lawyer at Baggett Law Personal Injury Lawyers.

-

File a claim under your Uninsured Motorist coverage.

FAQ Section

What is the average cost of car insurance in Jacksonville, Florida?

The average cost of car insurance in Jacksonville is $3,150 per year for full coverage. Minimum coverage policies average $1,380 per year.

How can I lower my car insurance in Florida? Why is insurance so high?

You can lower your car insurance by increasing your deductible and maintaining a high credit score. Insurance is high due to frequent hurricanes and a high rate of litigation in the state.

How long can you go without car insurance in Jacksonville?

You cannot go any amount of time without car insurance in Jacksonville if your vehicle is registered. Florida has no grace period for insurance lapses.

What happens if I don’t have PIP coverage in Florida?

If you don’t have PIP coverage, the DMV will suspend your driver’s license. You will also be personally responsible for your medical bills after an accident.

What happens if I don’t have car insurance in Jacksonville?

Driving without car insurance leads to a $500 reinstatement fee and a license suspension. If you cause an accident, you may face a lawsuit from a Jacksonville car accident lawyer.